Are you wondering what will happen to the Sydney property market in 2022?

Well … Sydney finished up the second strongest performing Australian housing market in 2021 with many locations experiencing 25+% house price growth.

Of course, the Sydney property market has been one of the strongest and most consistent performers over the last four decades.

Sydney property values:

- have stabilized with no growth in the last week,

- up 0.2% in the month to date, and

- increased 25.8% over the last year.

However there is still plenty of growth left, but the rate of price growth is now slowing with a flood of new property listing now hitting the market giving buyers more choice.

Having said that, there are still not enough good properties for sale to meet the extremely strong demand for houses in Sydney, particularly in the inner and middle-ring more affluent suburbs.

Yet the surge in supply of properties for sale gave buyers more choice and took a further edge off auction clearance rates and house price growth as the year came to and end.z

And it’s not just for houses…

Well located, family-friendly apartments in Sydney’s inner suburbs are likely to continue to perform strongly due to increasing demand from owner-occupiers and investors, however apartments in high-rise towers will continue to languish.

Real estate in Sydney’s larger regional locations, and in particular in lifestyle locations like Byron Bay, the Central Coast, the Hunter Valley, Wollongong, New South Wales south coast should also continue to perform strongly with beachside suburbs likely to outperform the wider overall market,

More investors are getting into the Sydney market now recognising that there are no bargains to be found, but that in 12 months time the properties they purchase today will look like a bargain.As you can see from the chart below, the Sydney housing market has notched up a gain of 4.3% in the last quarter alone and is headed for 25%+ capital growth this year.

SYDNEY DWELLING PRICE TRENDS – Source: Corelogic December 2021

Sydney’s new listings lifted strongly as the spring selling season got underway.

Source: Realestate.com.au Listings Report October 2021

The strength of the Sydney property market is also highlighted by the consistently strong auction clearance rates exhibited every weekend this year.

Sydney property buyers have been lured back into the market by low-interest rates, pent up demand, as well as a strong rebound in consumer confidence buoyed by a road map out of Sydney’s Coronavirus Cocoon.

At the same time rents have risen for Sydney houses in particular but rents are still flat in Sydney’s high rise apartment market segment.

So…is it the right time to get into the Sydney property market?

Now I know some potential buyers are asking “How long can this last? Will the Sydney property market crash in 2022?”

They must be listening to those perma bears who have been telling anyone who is prepared to listen that the property markets are going to crash, but they have said the same year after year and have been wrong in the past and I will be wrong again this time.

Recently both all our major banks have updated their property price forecasts in response to the market’s resilience in the face of extended lockdowns.

Westpac sees the Sydney property market growing 27% in 2021 and 6% in 2022.

Of course, over the past year, Australia’s property market values have increased at rates not seen in over a decade, and Sydney has led the charge.

This has been good news for homeowners but heartbreaking for house hunters.

At the same time, there have been mixed messages in the media about what’s ahead.

There’s always the Negative Nellies wanting to tell anyone who is prepared to listen to them the market is about to crash, but other more solid commentators are suggesting our property market is slowing down.

And I agree, I believe the pace of capital gains has peaked, but I’m not suggesting home values are about to dip, far from it.

Rather I believe we’ve moved from a peak rate of growth to a pace of capital gain that will be more sustainable and there’s plenty of life left in the Sydney real estate market with property values likely to keep increasing throughout 2022 and into 2023.

Australia’s economy seemed like it was going to experience that V shape recovery everybody had been was hoping for, but that was put on hold by the lockdowns in Sydney caused by the resurgence of coronavirus, but now that this is coming under control we’re likely to see strong economic growth and employment growth and this financial security will underpin Sydney property market moving forward.

When the international borders eventually open Sydney will be a favourite destination for students and highly skilled workers and this will put another “rocket” under the Sydney housing market.

However, some sectors of the Sydney property market will continue to languish.

The sectors of the Sydney real estate market likely to underperform most moving forward will be:

- Apartments in high-rise towers – in fact, this is these properties are likely to be out of favour for quite some time.

- Off the plan apartments and poor quality investments stock (as opposed to investment-grade) apartments, particularly those close to universities.

- Homes in the outer suburban new housing estates, where young families are likely to have overextended themselves financially and with many people will be out of work for a while. Currently, many first home buyers are taking advantage of the various incentive packages including HomeBuilder to buy newly constructed homes, leaving established houses in these locations languishing.

This means that you can’t just buy any property and count on the general Sydney property market to do the heavy lifting over the next few years, so careful property selection will be critical.

To help give you a better understanding of what’s really going on I’m going to explore the nitty-gritty behind Sydney’s market trends, the areas where long-term growth is still likely, and the impact of shifting demographics on the city’s future performance.

So how long will this cycle continue?

I see Sydney’s property market continuing growing at the rate of 6 to 7% per annum throughout 2022 until eventually, affordability slowed the market down.

Remember the current strong upturn phase of the property cycle only commenced in October 2020.

Normally the upturn stage of the property cycle lasts a number of years and is followed by a shorter boom phase which is eventually cut short by the RBA raising interest rates or by APRA introducing macroprudential controls to dampen the exuberance of property investors and home buyers.

However, this time around we have experienced an unprecedented rate of growth seeing our property markets perform even more strongly than anyone ever expected, with the rates of house price growth at levels not seen for a number of decades.

While a lot has been said about the 20% increase in property values many locations have enjoyed so far this year, it must be remembered that the last peak for our property markets was in 2017 and in many locations housing prices remain stagnant over a subsequent couple of years and it was really only early in 2021 that new highs were reached.

This means that average price growth was unexceptional over the long term, averaging out at around 4 per cent per annum over the last 5 years

But recently there seems to have been a change of sentiment about our housing markets from our financial regulators, the banks and even our treasurer.

The Council of Financial Regulators, the club of four main financial watchdogs, showed concern about the increased level of home lending in the first half of the year.

In particular, they signalled their concern about the number of mortgages taken out at more than six times the borrower’s income.

The council has asked APRA to put together a list of potential measures, but this is going to be a challenge and their response will need to be measured so as not to create unintended consequences such as a severe property downturn.

Just look back to 2014 when APRA checked house price growth by targeting investors and restricting the size of what they could borrow relative to the value of their housing collateral.

While tougher lending standards will certainly take some heat out of Australia’s property markets by restricting the number of people that can get home loans, or lessening the amount they can borrow, the move could backfire in the short term as investors and homebuyers try to rush and buy to beat the buzzer on the upcoming tightening of lending conditions.

Back to the question of when will this property cycle end – there is little doubt that Macro-Prudential controls will have a negative impact on our property markets and slow the rate of growth of housing values.

After all, that’s what they’re intended to do.

Whether the markets will just experience slower growth or stop dead in their tracks will depend on what measures are introduced.

Targeting debt to income ratios will have a limited impact on higher wealth households, who often have multiple streams of income.

However, it will affect lower-income households and those purchasing property for the first time.

If you think about it, first home buyers don’t have a “trade-in” of a previous home and therefore need to borrow higher loan to value ratios.

On the one hand, the government says it wants to encourage first home buyers, and on the other hand, it is encouraging the regulators to sideline them.

So in the meantime, it’s just a matter of ‘wait and see’ what our regulators choose to do.

I hope they have learned from the results of previous interventions, otherwise, if history repeats itself, there will be some unintended consequences.

Watch this space.

Fast facts about the Sydney Property Market

Sydney House Prices

Let’s start with a bit of history… Sydney property values have grown more than 400% in the past 30 years.That’s the cost of living in an international city on the water which offers an unparalleled lifestyle.

During the pandemic Sydney housing prices dropped by only 2.2%, demonstrating some resilience in the face of uncertainty.

And now in 2021, we are seeing the Sydney property market soar ahead.

Sydney is home to Australia’s 20 most expensive postcodes

Waterfront locations and coveted school zones dominate the country’s most expensive postcodes, Domain data shows.

All the postcodes in the top-20 list were in Sydney, led by the eastern suburbs, the northern beaches and the north shore.

Sure there are fewer good properties for sale at the moment, and almost all the good ones are for sale off-market, however, if you’d like to know a bit more about how to find these investment gems give the Metropole Sydney team a call on 1300 METROPOLE or click here and leave your details.

To help you understand what’s ahead for Sydney property I’m going to provide you with a lot of detail but the bottom line is Sydney is a world-class city, which is landlocked with limited room to grow to accommodate all those moving to Sydney looking for somewhere to live.

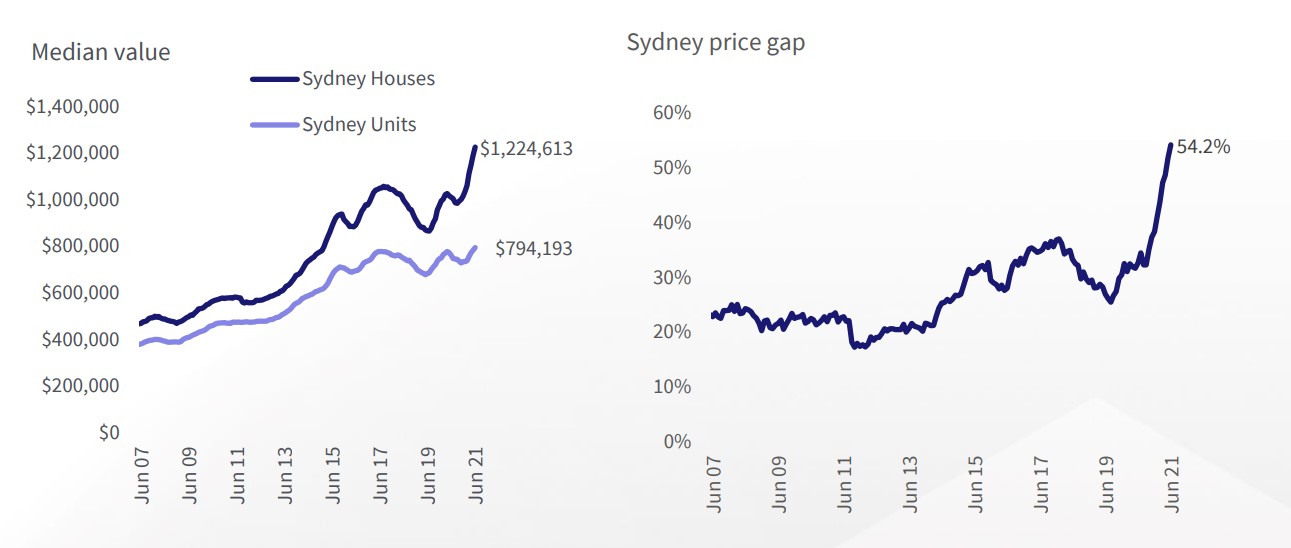

Sydney houses are outperforming apartments

Sydney is seeing a record high in the difference between house and unit medians at 52.4% as of June.

The difference in median house and unit values has skyrocketed since September 2020, as the housing market saw a recovery trend following eased social distancing restrictions across the city.

Unit values continued to decline through to January 2021, as low levels of investor participation, and subdued rental conditions saw less interest in unit stock.

As the Sydney lockdown reinforces the lasting impacts of COVID-19 on large cities, and monetary policy remains accommodative, Sydney-siders who can afford it may still be willing to fork out a premium for detached housing in the months ahead.

Sydney’s Property Market Trends

Historically, the city’s property market has gone from strength to strength.

Over the last 40 years, Sydney’s average capital growth was 7.4% meaning many properties doubled in value every decade.

And now the Sydney housing market is on the move as can be seen by the rise in asking prices:-

Source: SQM Research

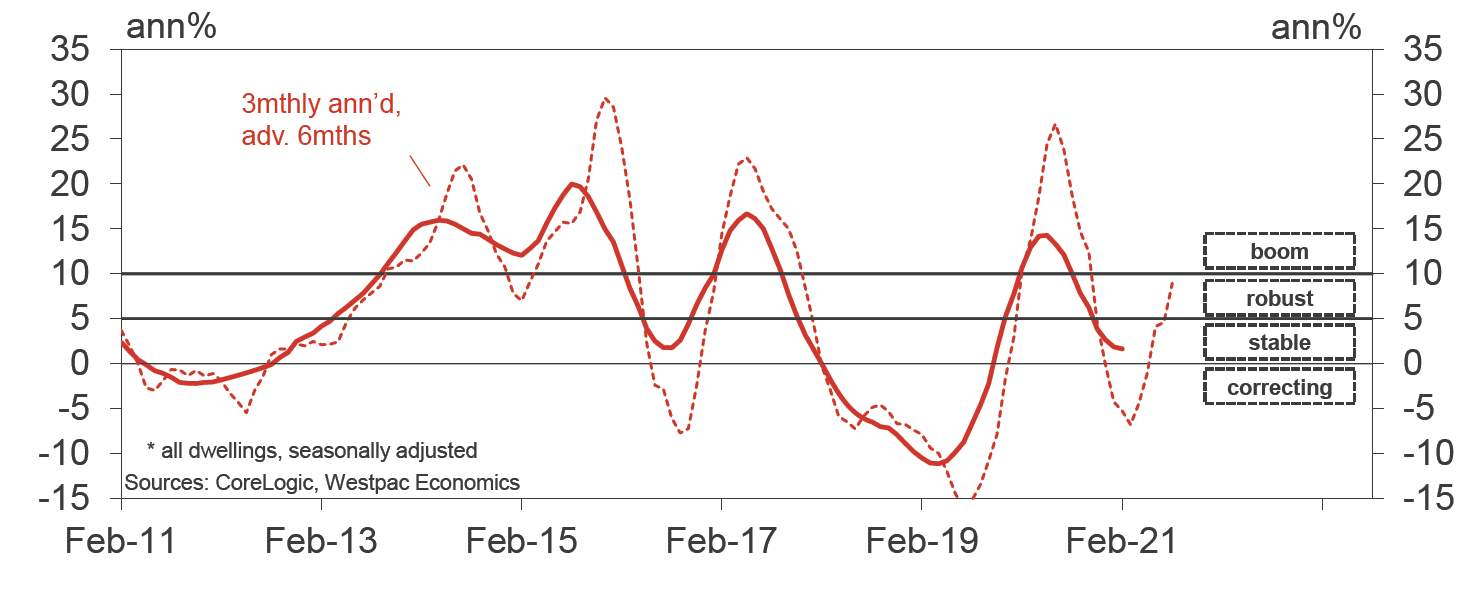

The following chart shows how well Sydney dwelling fared through last year’s CoronaVirus pandemic.

The Sydney Apartment Market

Sydney has embraced apartment living more than any other Australian capital and family suitable apartments are seen as an affordable alternative to houses and units in popular areas such as Sydney’s eastern suburbs and Northern Beaches, where they are likely to enjoy continuing strong demand which will result in a strong increase in values.

On the other hand, apartments in high supply areas present a significant risk to property investors.

This trend already occurred prior to COVID-19 where certain areas in Sydney experienced major unit oversupply.

It seems the property investors are slowly understanding the risks associated with high-rise tower apartments in Sydney including potential construction defects, high vacancy rates, lack of scarcity, lack of capital growth and the challenges of buying in buildings that are predominantly owned by investors, and often many overseas investors.

On the other hand, family-friendly apartments in medium and low rise buildings within Sydney’s inner and middle-ring suburbs are likely to perform well as investments.

With capital growth in houses outperforming apartments so far this year, the pricing gap between houses and apartments is around 50%, so I see increasing demand for these more affordable apartments moving forward.

This will be partly driven by investors returning to the market, so by first home buyers who are being priced out of standalone houses in Sydney.

Prior to Covid-19 metropolitan Sydney required about 41,000 additional dwellings per annum to accommodate its population growth which was underpinned by overseas and interstate migration.

To meet this demand the delivery of new apartment projects was vital, particularly as affordability pressures, demographic trends, changing household types and lifestyle preferences drive the need for more diverse housing options.

And then came CoVid19…

But the new apartment market was already feeling the effects of a downturn in Off-the-Plan (OTP) purchaser demand.

The following graphics from valuers Charter Keck Kramer give a good picture of what’s currently happening in Sydney’s apartment market

{kind=link}

The closure of international borders has caused a significant reduction in tenant demand as net overseas migration inflows effectively fell to zero.

So far, the owner-occupier market is holding up, supported by low-interest rates, which have improved affordability for those with jobs.

First, home-buyer demand is being encouraged by stamp duty concessions.

In turn, this is supporting demand for affordable apartments that are suitable for owner-occupiers.

Both upgraders and downsizers remain active where they are transacting within the same market.

Over the last few years, an apartment oversupply and other regulatory and non-regulatory factors have resulted in the collapse of investor demand for Sydney “off the plan” apartments.

The reduced sales volumes have made it more difficult for developers to achieve the pre-sale hurdles required by the banks to finance developments, and a few new projects are on the drawing board.

This means that undersupply of apartments is looming.

But be careful – many of the new Legoland apartment high-rise towers will always remain secondary quality and become the slums of the future – steer clear of these.

The looming undersupply of new projects will lead to lower vacancy rates, rental growth, and eventually, property price growth of these new apartments and in turn, will help fuel increase price growth of well-located establish a purpose in Sydney.

House prices have risen across most school catchment zones analysed, with 89% of primary and 95% of secondary schools increasing annually, aligning with the rising property market.

While the top school catchment zones were spread across inner, middle, and outer suburbs, many that topped the list favoured lifestyle locations, spanning coastal suburbs or near to national parks.

House price growth varied between neighbouring school zones. House prices in Balgowlah Heights Public School catchment zone jumped 33% annually, while the neighbouring school zone of Manly West Public School dropped 7.9%.

Domain’s chief of research Nicola Powell said the pandemic had helped supercharge school catchment prices with flexible working allowing young families to relocate to suburbs with easy access to beaches, parks, and schools.

“It’s astonishing to see that starting on a high base of house prices, one-in-10 school catchment zones are achieving 10 to 20 per cent more than the suburb they are located in,” Powell said.

We know that as part of the property decision-making process, parents and investors consider the geographical location of a potential property in relation to a school catchment zone.

When people are looking for a home, they’re looking for a lifestyle, and education is a big part of that picture, be it in the inner-city suburbs or the coastal regions of Australia.”

Dr. Powell explains that the boundary of a public school catchment is often a critical factor when it comes to purchasing a family home.

In Sydney, secondary school catchments appear to have a more positive impact on house price growth compared to primary school catchments.

Which catchment areas come out on top for Sydney?

Here’s the list of the top 10 Sydney high schools catchment areas:

| school name | median | yoy | ||

|---|---|---|---|---|

| 1 | Barrenjoey High School | $2,802,500 | +45.0% | View CatchmentsView |

| 2 | Cronulla High School | $2,030,000 | +40.0% | View CatchmentsView |

| 3 | Kogarah High School | $1,300,000 | +38.4% | View CatchmentsView |

| 4 | Kincumber High School | $1,175,000 | +38.2% | View CatchmentsView |

| 5 | Woolooware High School | $1,610,000 | +34.2% | View CatchmentsView |

| 6 | Mosman High School | $4,000,000 | +33.3% | View CatchmentsView |

| 7 | Seven Hills High School | $942,500 | +31.4% | View CatchmentsView |

| 8 | Davidson High School | $1,800,000 | +30.0% | View CatchmentsView |

| 9 | Wyong High School | $600,000 | +29.7% | View CatchmentsView |

| 10 | Killara High School | $3,200,000 | +28.3% | View CatchmentsView |

Source: Domain

Here’s the list of top 10 Sydney primary school catchment areas:

| school name | median | yoy | |||

|---|---|---|---|---|---|

| 1 | Burraneer Bay Public School | $2,100,000 | +44.8% | View CatchmentsView | |

| 2 | Newport Public School | $2,675,000 | +43.0% | View CatchmentsView | |

| 3 | Woy Woy Public School | $870,000 | +41.5% | View CatchmentsView | |

| 4 | Kellyville Ridge Public School | $1,377,500 | +37.8% | View CatchmentsView | |

| 5 | Harbord Public School | $3,050,000 | +37.6% | View CatchmentsView | |

| 6 | Kincumber Public School | $912,500 | +36.9% | View CatchmentsView | |

| 7 | Belmore North Public School | $1,350,000 | +35.3% | View CatchmentsView | |

| 8 | Hurstville Grove Infants School | $1,425,000 | +33.8% | View CatchmentsView | |

| 9 | Casula Public School | $845,000 | +33.6% | View CatchmentsView | |

| 10 | Balgowlah Heights Public School | $3,225,000 | +33.0% | View CatchmentsView |

Source: Domain

NOW READ: The 15 Best Suburbs to Invest in Sydney in 2022

Sydney’s Rental Market

While over the long term rentals have grown in line with property values, more recently rental growth has slumped, in part due to the influx of rental properties that were previously let on short-term leases such as AirBnB and student accommodation.

As a consequence, overall yields have declined as can be seen from the following chart from SQM Research.

Traditionally in Sydney, vacancy rates have been tight; hovering well below the level of 2.5% vacancies, which traditionally represents a balanced rental market.

However currently the overall vacancy rate in Sydney has crept up to close to 4%, but this varies in different locations.

At Metropole Property Management our vacancy rate is less than half this rate, in part because our clients have chosen investment-grade properties, but we’d like to think it also has a bit to do with our proactive property management policies.

Sydney’s Average Capital Growth

In 1993, the average house price in Sydney was $188,000.

However, dwelling price growth in Sydney has been very fragmented.

While some suburbs has just chugged along others are strongly outperforming.

You see…Sydney is comprised of dozens of smaller markets, each of which has its own drivers and supply/demand issues.

Sydney’s more affluent inner eastern, Lower North Shore, and inner western suburbs have well outperformed these averages.

Houses: In September 2019, only 5% of Sydney suburbs had a median house value lower than $500,000, compared with 22% five years ago.

The proportion of suburbs with a median house value of $1 million or higher was 47% in September 2019, up from 34% five years ago.

Units: 29% of Sydney suburbs recorded a median unit value of $500,000 or less in September 2019, down from 49% five years ago.

The proportion of suburbs with a median value of $1 million or higher jumped from 2.9% five years ago to 14.4% in September 2019.

Overall Sydney is a city in gentrification, with the fingerprints of a younger demographic upping the desirability of the city lifestyle.

Houses and apartments in Sydney’s easter, inner west and lower North Shore suburbs offer the best prospects of long term capital growth as this is where there are more Skill Level 1 worker – those who earn higher incomes, often having multiple sources of income.

Fact is, the rich are getting richer and they are able to and prepared to pay more for their homes

In its relatively short history, Sydney experienced near starvation, rebellion attempts, a gold rush, trade booms, the Great Depression, two world wars, and hosted the Summer Olympics.

Article by https://propertyupdate.com.au/